Introduction

The landscape of modern work has undergone a seismic shift over the past decade. The traditional nine-to-five office model is no longer the sole pathway to a successful, high-paying career. Today, millions of professionals have embraced the digital nomad lifestyle, combining remote freelance work with global travel. While this geographic independence offers unparalleled personal and professional freedom, it also introduces a highly volatile set of risks. From sudden medical emergencies in foreign countries to stolen high-end laptops, data breaches, and unexpected trip cancellations, the vulnerabilities of working on the road are substantial.

Traditional insurance policies, designed for static residents with long-term domestic contracts, fail to meet the dynamic needs of this demographic. This critical gap in the market has paved the way for a revolutionary financial solution: on-demand micro-insurance for digital nomad freelancers. This specialized, tech-driven insurance model offers flexible, short-term, and customizable coverage tailored specifically to the fluid lifestyle of remote, self-employed professionals.

Why Traditional Insurance Fails the Modern Nomad

Traditional insurance models are inherently rigid. They typically require annual commitments, static geographical declarations, and extensive underwriting processes that do not align with the life of a modern freelancer. For a digital nomad who might spend three weeks in Colombia, a month in Thailand, and then return to their home country for a short holiday, legacy policies are both impractical and prohibitively expensive.

Furthermore, conventional plans rarely cover the specific tools of the trade for digital professionals. A standard travel insurance policy might cover lost luggage up to a small limit, but it often caps payouts for high-end electronics like laptops, cameras, microphones, and tablets—the very tools that allow a digital nomad to generate income. Consequently, freelancers are left either overpaying for international commercial insurance they do not fully utilize or carrying significant uninsured risks that could derail their entire business operations in a single day.

Understanding On-Demand Micro-Insurance

On-demand micro-insurance for digital nomad freelancers represents a complete paradigm shift in risk management. Built on digital-first insurtech platforms, these insurance solutions allow freelancers to purchase highly specific coverage only when and where they need it. Instead of a blanket annual policy, a freelancer can opt for a weekly health plan while hiking in Patagonia, or a single-day liability cover when executing a high-stakes client workshop.

The ‘micro’ aspect refers to both the granular nature of the coverage and the affordable pricing structure. By stripping away unnecessary extras, insurtech providers can offer hyper-targeted coverage at a fraction of the cost of traditional plans. Activation is typically instantaneous via intuitive mobile apps, allowing users to toggle coverage on or off with a simple swipe on their smartphones. This pay-as-you-go security ensures that nomads are never paying for insurance they do not actively need.

Key Coverage Pillars for Digital Nomads

When evaluating on-demand micro-insurance for digital nomad freelancers, it is essential to understand the core pillars of protection that these modern policies address:

1. International Health and Medical Cover

Unlike standard travel insurance which only covers emergency medical evacuation, nomadic micro-health insurance provides comprehensive medical care abroad. This includes routine doctor visits, dental emergencies, mental health support, and coverage for local treatments, ensuring freelancers do not have to fly back home to receive essential medical care.

2. High-Value Tech Equipment Protection

Digital nomads rely heavily on specialized, expensive hardware. Micro-insurance plans allow freelancers to register their specific devices (e.g., MacBooks, DSLR cameras, drawing tablets) online and insure them against theft, loss, or accidental damage worldwide. Some premium providers even offer rapid replacement services to minimize business downtime.

3. Professional Liability and Indemnity

Freelancers face legal and financial risks from their clients. If a remote software developer accidentally deletes a client’s critical database, or a copywriter faces a copyright lawsuit over an accidental plagiarism claim, professional liability micro-insurance provides short-term legal defense and compensation coverage for the duration of that specific project contract.

4. Cyber Security and Data Breach Insurance

Working from public Wi-Fi networks in co-working spaces and cafes leaves digital nomads highly vulnerable to cyber threats. Micro-insurance policies now offer coverage for losses incurred due to ransomware attacks, identity theft, and accidental data breaches affecting client information.

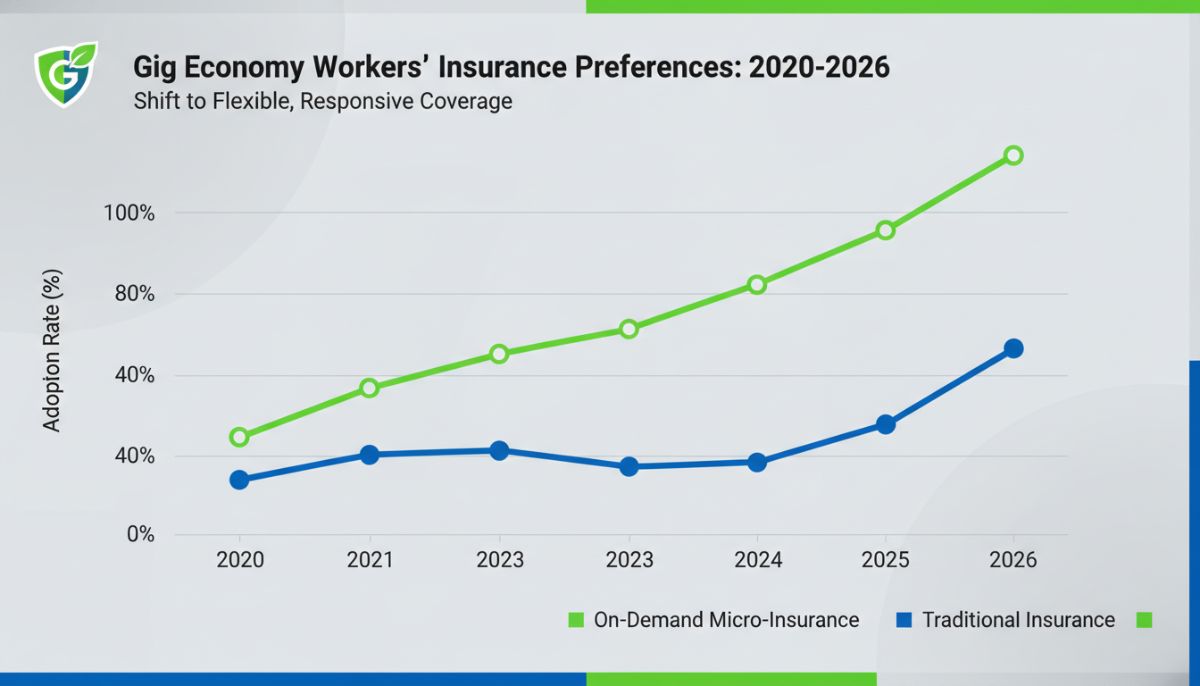

Comparative Analysis: Traditional vs. On-Demand Micro-Insurance

To illustrate the stark differences, let us examine how these two models compare across key parameters essential to the nomadic lifestyle:

| Feature | Traditional Insurance | On-Demand Micro-Insurance |

|---|---|---|

| Contract Duration | Minimum 1 year commitment | Daily, weekly, or monthly (Flexible) |

| Geographical Scope | Static / Single country focus | Global (Multi-country transit supported) |

| Tech Equipment Limits | Low caps, often excludes commercial gear | High caps, tailored for professional tools |

| Activation Speed | Days to weeks (Paperwork required) | Instant (Mobile App / Digital platform) |

| Pricing Structure | High fixed monthly/annual premium | Pay-as-you-go, micro-premiums |

| Cancellation Policy | Penalties or complex termination | Toggle off anytime without any penalty |

| Professional Liability | Rarely included in personal travel plans | Available as an on-demand add-on |

The Strategic Value of Pay-As-You-Go Security

For freelancers, cash flow can be highly volatile. During months of high client acquisition, investing in robust protection is easy. However, during leaner periods, fixed expenses can become a heavy burden. On-demand micro-insurance aligns perfectly with the variable income streams of the gig economy.

“The future of financial security lies in adaptability. For the digital nomad, an insurance policy must be as agile as their travel itinerary. On-demand micro-insurance is not just a safety net; it is an enabler of global professional freedom and business continuity.”

By allowing freelancers to adjust their premiums based on their current location, project load, and travel schedule, micro-insurance acts as a catalyst for sustainable remote careers. It democratizes access to safety nets that were previously only available to corporate employees, leveling the playing field for independent contractors globally.

How to Choose the Best Micro-Insurance Provider

As the insurtech market expands, several specialized platforms have emerged. When choosing a provider for your nomadic business, consider the following criteria:

- Global Underwriting Network: Ensure the provider has a strong global network of medical and logistics partners to guarantee seamless claim payouts in foreign jurisdictions without language barriers.

- Claims Processing Speed: Look for platforms that leverage automated claims processing (often powered by AI) to ensure you are reimbursed quickly, reducing out-of-pocket expenses.

- Customization Options: The ideal platform should allow you to customize your coverage dynamically. You should be able to add professional indemnity or equipment coverage to your core health plan seamlessly during a busy project.

- Transparent Exclusions: Always read the fine print regarding high-risk adventure sports, specific geographical exclusions, or pre-existing medical conditions to avoid unexpected denials of coverage.

Conclusion

The boundary between work and life has permanently dissolved for the modern freelancer. As the digital nomad ecosystem continues to mature, the tools supporting it must evolve in tandem. On-demand micro-insurance for digital nomad freelancers represents a critical evolution in financial services—one that champions flexibility, affordability, and comprehensive protection. By shifting from rigid, outdated policies to agile, digital-first solutions, remote professionals can focus on what they do best: creating, innovating, and exploring the world with absolute peace of mind.